Open ING or N26 current account?

Overview

You do not open a current account every day. Therefore, it is meaningful to take the decision of choosing the provider prudentially.

The comparison as well as the experiences and tips of the editorial and community will help you finding the best option for you, open the account successfully and coping fast with the new bank.

Comparison:

Take a look at the points that are important for you

ING |

N26 |

|

| Account management fee per month including all transactions, standing orders, etc. |

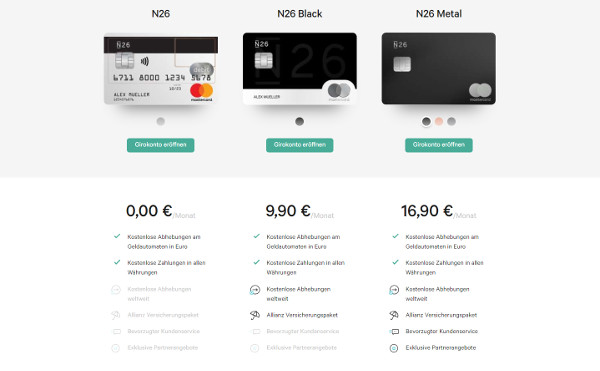

free of charge! | free of charge (fee-based upgrades are possible, not included in the comparison) |

| Application | ► online | ► online |

| Cards | ||

| Visa Card |  Visa Card (free of charge) |

Mastercard (free of charge) |

| 2nd Card |  Girocard (free of charge) |

solely Maestro Card (free of charge) |

| Overdraft facility / Credit line | ||

| initial credit line (immediately after application) |

up to € 500 (based on the determined creditworthiness) |

up to € 1,000 (based on the determined creditworthiness) |

| maximum credit line | up to € 10,000 (3-times the salary, submit the proof of salary) |

up to € 10,000 (actual salary, creditworthiness assessment) |

| Can the credit line be increased through deposits? | yes (millions are possible) |

|

| Why is that important? Both banks keep it simple: There are no additional settlement accounts for the cards. No matter which card you use, it is always debited from the current account (debit system). That means for you: The account balance possibly plus the overdraft facility is the credit line for account and cards. |

||

| Credit card payment | ||

| Fee for payments in Euros | free of charge | |

| Fee for payments in foreign currencies | 1.75 % | 0.00 % |

| Cash supply | ||

| Withdrawing from the ATM Germany + rest of the world |

free of charge, wherever the Visa Card is accepted | free of charge, wherever the Mastercard is accepted |

| Limits? | at least Euros 50 per withdrawal | 3 or 5 times per month free of charge, then € 2 per withdrawal |

| Surcharge at foreign currencies? | 1.75 % | 1.70 % |

| Are you frequently in the foreign currency abroad? There are providers without foreign transaction fee | ||

| Account management and communication | ||

| online banking | yes | |

| app banking | yes | |

| telephone banking | yes Mon–Sun around the clock |

no |

| Availability of the customer service | through phone (069.50500105), e-mail, contact form Mon–Sun around the clock |

through app chat Mon–Sun around the clock |

| Supplementing services | ||

| Apple Pay | starts 2019 | yes |

| Google Pay | no | yes |

| Optional joint account or authorized persons | yes | no |

| Call money (savings account with immediate availability) | yes Extra-Konto |

no |

| Fixed deposit (savings account with term) | yes | yes |

| VWL-Sparen (federally supported saving for certain income groups) | yes | no |

| Depot | yes, very extensive | mini-funds solution |

| Installment loan | yes, from € 5,000 to 50,000 | yes, from € 1,000 to 25,000 |

| Further financing possibilities | • car loan • credit line • housing loan • construction financing |

no |

| Account opening | ||

| Place of residence | Germany | Germany or Austria, Spain, Italy, Ireland, France, Greece, Slovakia |

| Legitimating | VideoIdent or PostIdent | |

| Really free account opening? | yes | |

| Open current account: |  www.ing.de |

www.n26.com |

| Please give me feedback using the comments feature about what current account you decided for and also the reason why. This way, we can better dive into the smart use (tips and tricks) in following articles. A heartly thanks for choosing DeutschesKonto.ORG for your research! |

||

Experiences

Fully developed and functional banking app

ING Current account

I have my own free current account at the ING since the 28th of January 2008. A long timeframe, isn’t it?

The ING is a solid, long-established, however modern bank. Formerly, when there were no “FinTechs” like N26, it has co-designed the development with telephone banking and BTX banking.

Today, it waits to see what FinTechs are doing. If it proves itself, ING will take it on, as with Apple Pay in the year 2019.

With more than 9 million customers, the effort and the result is higher when innovations are implemented.

At the same time, it is crucial to combine innovations with the long-established. Therefore, the ING is one of the few banks where you can still do telephone banking. This is especially valued by elderly persons, for example my mother!

The ING is a bank to which you can switch completely!

The ING has included everything, from the current account to savings accounts and depot up to several types of financing. The customer service as well as the availability (!) of the customer service are very good through the several offered channels!

I salute the bank that it can maintain the quality in spite of the high number of new account openings. The ING has acquired more than 600,000 customer in the past year.

More than 1,600 times a day, the decision is:

Yes, I open my account at the ING!

My mother and I are very happy that we have a current account at the ING. She primarily uses the telephone banking and I the online banking.

Extensive, but tidy online banking system

N26 Current account

The N26 current account can be especially regarded as a supplement to another bank. In spite of the fee-based premium services, the bank, which startet in 2015, cannot cover all areas.

Further meaningful settings, including Google Pay!

However, it is ahead of other banks in other points – such as Google Pay, Apple Pay, cash deposits through shops. This also applies to the app in combination with the cards and the account management.

The cards can be blocked and unblocked again, e.g. for different transactions. The account transactions can be shown immediately on the Smartphone or iPhone, if desired with a push-notification.

This is thrilling for young people, who love to have all the information at all time and therefore, full control of their finances.

Always immediate control of the finances

A little disadvantage is the customer service, which is now only available through the app. This saves costs for the bank, of course, but is not the best for everyone.

N26 does not want to be the bank for everyone, but wants to attract especially technology-open people.

Who engages him/herself will become a customer at one of Europe’s most modern banks for free and can look forward to be on board of the most recent innovations.

We have some people in our community, who use N26 as their main current account … however, my personal recommendation is to hold at least another very good current account as a backup solution. Agreed?

If you are willing to pay account management fees, you get insurances on top. Who needs it? Background is that the insurance group Allianz is an investor at N26.

Account opening

The account opening is pretty easy at both providers. At the ING as well as at the N26, it is a continuous procedure to make the account opening as easy as possible.

That’s obvious: One wants to turn an acquired interested person into a customer of many years. This is why the online application is very self-explainatory and compared to the procedures of account openings of other banks, it is fast and easy.

You enter your personal data and contact information. In the next step, the provider checks your creditworthiness in an electronical manner and the “traffic light will turn green” in the best case.

You can make your legitimating through PostIdent or VideoIdent. For this purpose, you visit the post office with your ID-card or passport or hold your documents in front of the video camera. Both is tried, proven, safe and of course, for new customers free of charge.

As soon as this is done, the production of your cards starts. They will be shipped by mail.

Easier than many think!

Depending on whether you have applied for an overdraft facility at the account opening, you can use the cards immediately or make a transfer first in order to have balance in your account.

Which account did you decide for?

ING |

N26 |

|

| Account management fee per month including all transactions, standing orders, etc. |

free of charge! | free of charge (fee-based upgrades are possible, not included in the comparison) |

| Place of residence | Germany | Germany or Austria, Spain, Italy, Ireland, France, Greece, Slovakia |

| Legitimating | VideoIdent or PostIdent | |

| Really free account opening? | yes | |

| Open the current account: | www.ing.de |

www.n26.com |

Yes, you can also open both accounts. They supplement each other in many aspects. You are welcome to write me through the comments feature about how it is for you! Thanks. 😀🙏

If you start now, you are done in a few minutes, the rest will arrive by mail!

Tips for the account opening

- Start immediately

You know all data that you need for the account opening by heart (or it is saved in your mobile phone). Instead of postponing the opening of a new account again and again, start right now. - Data of income

Sum up all sources of income that you can proof. If you do not want to apply for an overdraft facility, you won’t be asked for the proof anyway. - Weak creditworthiness?

In this case, you can add a second account holder during the application procedure are the ING. Always take the person, who has the higher creditworthiness as the first account holder. If you do not know who it is, then take the person with the higher income. - Change of profession or place of residence?

Differently from the first advice, if possible always apply for a new current account, when you have a permanent income through a job or pension. If you think about a change of job, then imperatively apply for the account beforehand. This will bring you more creditworthiness points. The same applies to planned moving. Apply still using your old address (unless you move to a considerably better neighbourhood).

| Account management fee per month including all transactions, standing orders, etc. |

free of charge! | free of charge |

| Open current account: | www.ing.de |

www.n26.com |

Questions?

Questions are welcome to be asked through the comments feature. A heartly thanks to our great community, who helps other smart bank customers with own experiences and ideas!

Hi.. Good comparisons..I have both accounts with ING and N26.. I started N26 as a backup to the ING as i will have to pay the monthly fees… So far I have been able to avoid by moving money back and forth. ING has no fine print as of yet about abuse as N26 does with regards to the money coming in then leaving to make the monthly minimum.

That said. There are a few updates you have to do to this comparison..

ING.. Now required monthly deposits of 700€ to avoid the 4.90€ service fee. The now have Apple pay and Google Pay. Works well. Oh. You can hookup 2 devices no problem with the app.

N26.. Customers service is easily accessible via chat with hardly any wait- i like it! They also have a telephone number. I have not used it for banking but if you need to talk to them- its there.

The maestro card is now clear like the debit card and you require at least 100€ deposited to the account before you can order it.

Sign up was easy. Cards arrived in two days. Nothing else will come in the mail… You set your own pins when activating them.

Only one device will be fully paired. The second can access but requires 2FA via sms. The do not use authentication apps yet. I have changed my German registered number successfully to a US google voice number for both calls and 2FA to be able to use any device on the fly as i frequently swap sim cards between Canada, USA and Germany.

N26 does have a form of savings that is liquid.. They call them spaces. On basic free accounts you can create 2. You will get separate statements for them. You can delete and add them anytime. The Savings you listed that a term savings is actually setup via third party providers but is reported in the N26 app..

Now ING sent a letter with more changes… Here is one that might be major for some people.

Bezahlen in Ländern mit anderer Währung als dem Euro Für den Einsatz der girocard und VISA Card zum Bezahlen von Waren und Dienstleistungen in Ländern des Europäischen Wirtschaftsraums mit anderer Währung als dem Euro berechnen wir ein Auslandseinsatzentgelt von 1,99 % auf den Kaufbetrag. Bisher waren das 1,75 %. Das gilt auch in allen anderen Ländern mit Fremdwährung. Auch beim Geld abheben am Automaten im Euro-Ausland ändert sich etwas: Sollte der Betreiber Entgelte berechnen, werden diese nicht mehr von uns erstattet.