Apply successfully for the ING loan in Germany ✅

On this page, it is not about whether taking a loan is meaningful or not – you decide this for yourself!

This page helps you to get a loan in Germany!

Contents

Finally, your creditworthiness is the decisive factor.

As it is your creditworthiness, it is within your area of responsability to present your creditworthiness in the online application best possible (unfortunately, people make too many mistakes when entering the data) and if necessary, improve the creditworthiness before applying for a loan.

A) General requirements for the ING-loan

| Loan amount | Interest rate | Repayment phase | Particularities |

|---|---|---|---|

| € 5,000 up to 50,000 | ► show current interest rate | 1–7 years | early (partial)repayment possible at any time (special repayment) |

Requirements that you have to meet:

- Minimum salary of Euros 1,150, proven through:

- the last 3 salary slips at employees

- the last pay slips at officers, soldiers, judges

- the last pension notice (not older than 1 year) at pensioners

- the last 2 income tax notifications at self-employed persons

- Optionally: Increasing the creditworthiness through additional income (if it is a job, then through salary slip, alternatively through submitting the bank statements of the last 3 months)

- Minimum age of 18 years and place of residence in Germany

- Sign the original loan contract and send it with the mail to the bank (possibly with proof of salary)

- Legitimating in the post office or through video-chat

Alright so far?

Then let’s start:

B) Online application step-by-step

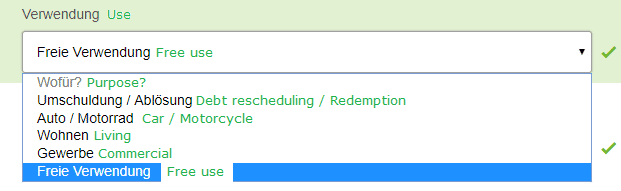

Choose the use of the loan amount

Preselected is “freie Verwendung” (free use). If you leave it that way, you do not have to send the bank a proof of the money use.

If you choose “Auto / Motorrad” (car/motorcycle) or “Wohnen” (living), you receive a cheaper interest rate, but you have to prove the use through a purchase contract (vehicle) or bills for the housing equipment/renovation. The subject debt rescheduling is tackled here and the ING does not offer commercial loans.

Loan amount

You enter here how much money you want as a loan. In the form, you can enter lower amounts than Euros 5,000 or higher than Euros 50,000, but the loan will not be provided by the ING (it currently only grants loans within the above mentioned amounts).

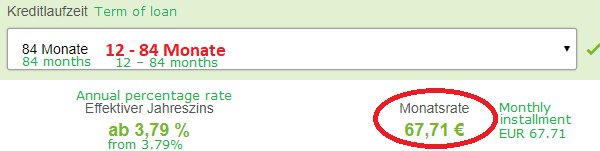

Term (duration of the repayment phase)

The longer the repayment phase (term), the lower the monthly installment.

Advice: The probability of a loan approval increases with the term. The ING grants loans up to 7 years (84 months) … even if you can state a longer term in the online application.

It is very practical that you are immediately shown the monthly installment.

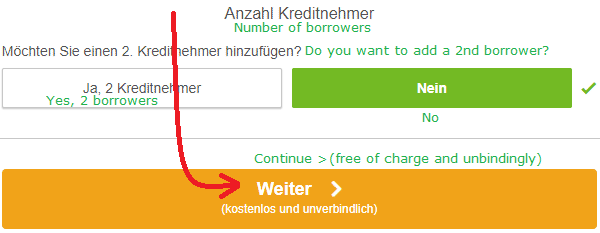

Number of borrowers

Preselected is that no further borrower is added. That means: you apply alone for the loan.

A 2nd borrower increases the creditworthiness, if a second income is included in the calculation. This is a classic case for married couples. However, you can also apply for a loan together with a different person. At the ING, these persons must be registered at the same address. If the second person does not have an own income (for example wife, who takes care of the children), then this won’t help. The borrower no. 1 should always be the person with the higher income.

Page 2

What’s your name and how can you be contacted?

Very easy: You state who you are and how to contact you.

Important: Enter all you given names and family names as stated on the ID or passport. This is important for the latter legitimating.

If your telephone number is not a German one, then you have to add the country code. For example 0048 for Poland (“00” instead of “+”).

Then you have to tick the first box; the second is voluntary, if you want to receive the newsletter and further offers (advertisement).

Page 3

Personal data

The first field is optional. The other fields are self-explanatory? If not, then just ask using the comments feature at the end of the page. Birth country and citizenship can be chosen from the menu.

Choosing the marital status only has an effect at “married”. All the other possibilities are calculated as “single”.

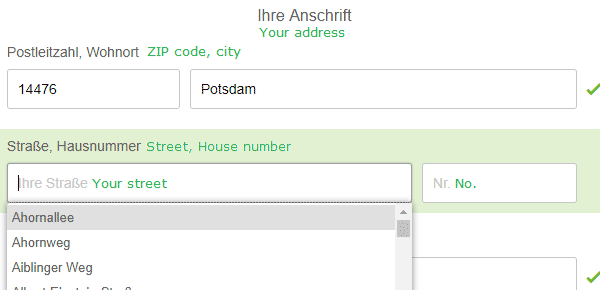

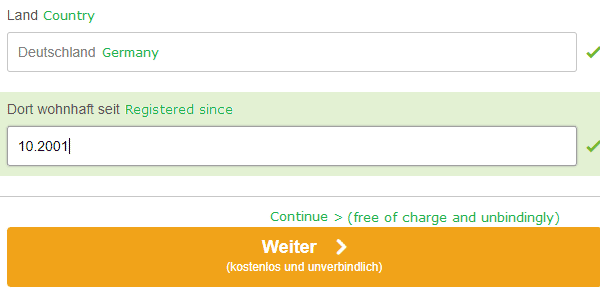

Address

When you enter your address, it is immediately verified.

At the country, “Deutschland” (Germany) is preselected and cannot be changed, as the ING does not grant loans to the abroad.

If you live less than two years at the current address, then you have to state the previous address too. For this, new fields open automatically.

Page 4

Variants are shown

In most cases, the loan application is not so long as shown here. We have embedded pictures and variants in order to have a big cover-up for our readers.

For example, no fields for pensioners are shown to you being an employee, and viceversa. 🙂

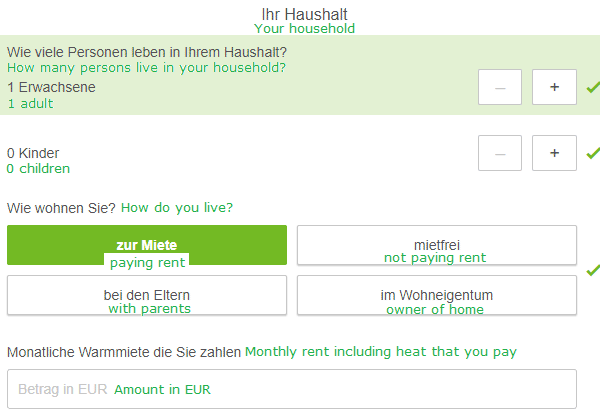

With how many people do you live together?

State how many adults and how many children live in your home.

Important: Only state the number of children for whom you receive child support or you have to maintain. A lump-sum is deducted for every person in the calculation, so that homes with few people have an advantage.

If you live “mietfrei” (not paying rent), you do not have to state further data. At “zur Miete” (paying rent) and “bei den Eltern” (living with parents), the costs for the appartment are stated – including the ancillary costs!

Who lives “im Wohneigentum” (owner of home), has to state further dara, such as square meters and possibly real estate financing.

Do you own real estate asset?

If you own real estate and earn income through it (income from rent), then please state it here. This increases the creditworthiness. If you do not have a property, then skip this field.

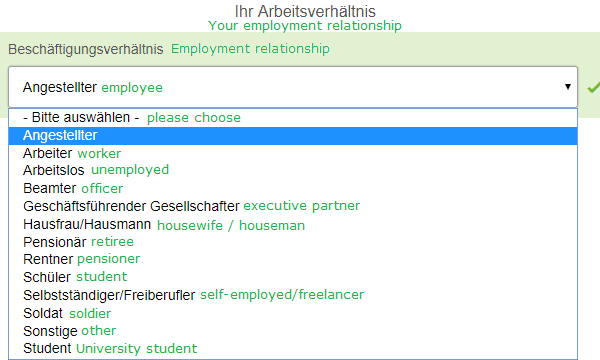

What’s your job?

Choose your employment contract. Arbeitslos (unemployed), Hausfrau/Hausmann (housewife/houseman) and Sonstiges (others) are the options with the worst chances!

How much do you work?

It is self-explanatory that a full-time job will give you many important points in the creditworthiness assessment. 😉

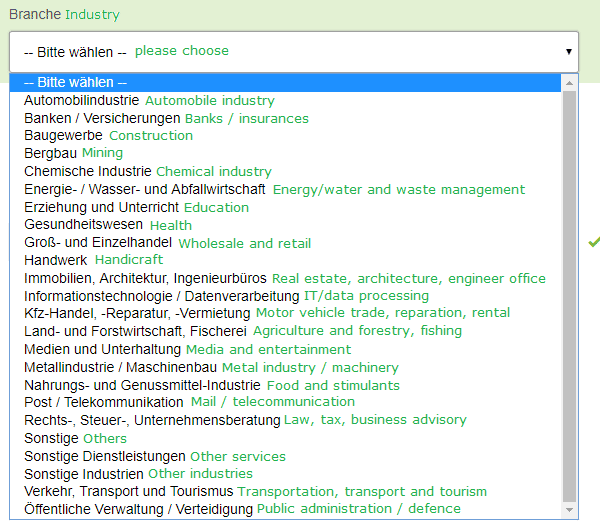

In which industry do you work?

If your industry is not named, then choose the most similar one. Handwerk/Handel (handicraft/merchandise) is a better term than Sonstige … (others) from the perspective of creditworthiness.

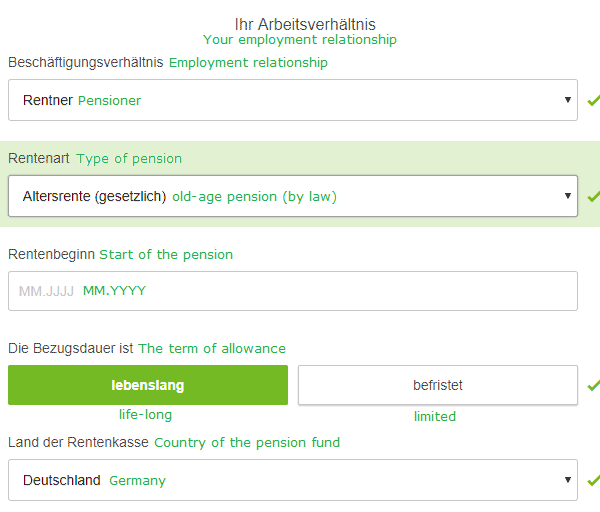

If you are a pensioner, this selection will open:

There are different types of pensions that you can choose above. Then you state the beginning of the pension and whether it is a permanent or limited pension, as well as the country from where the pension is paid.

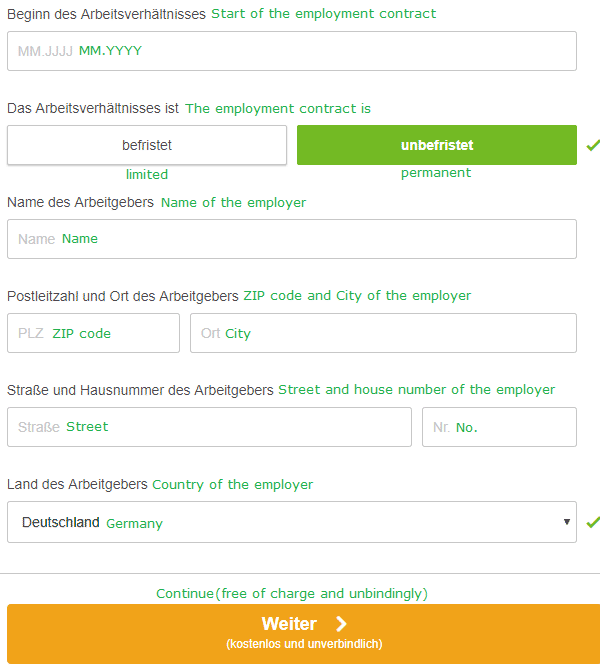

Where do you work and since when?

In the ideal case, you work permanently since at least 6 months or longer at that employer. This also applies to the second borrower. If this is not the case, then continue anyway. It is about the complete assessment!

The address of the employer also has to be stated.

Page 5

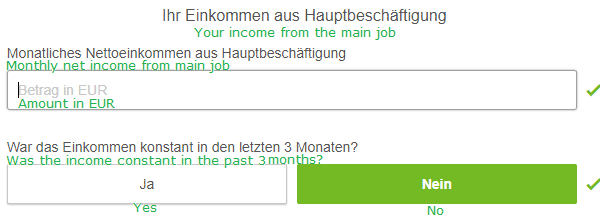

How much money do you earn? (main job)

State the monthly net income from your main job. This is often, but not always, the amount that is transferred to your current account (amount of payment). If the payments differ monthly, then state the lowest amount of the last 3 months and tick no at the question below ⟶ positive surprise for the loan processing!

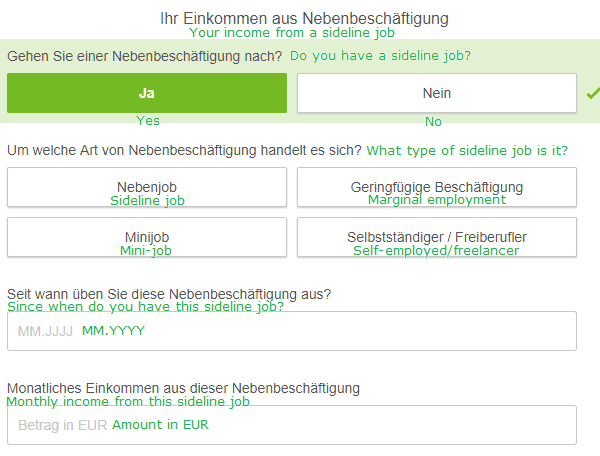

Do you have a sideline job? (…and earn from it)

Sideline jobs can vary a lot. If you click on the selection-buttons Nebenjob (sideline job), geringfügige Beschäftigung (marginal employment), Minijob (mini-job) or Selbstständiger / Freiberufler (self-employed/ freelancer), the selection below will change.

Important: Only state income that you can prove! As a proof, salary slips and/or bank statements are accepted.

Additional income increases the creditworthiness.

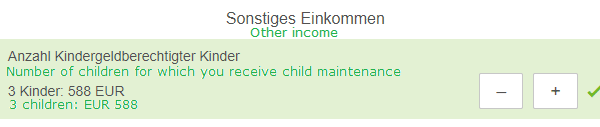

Do you receive child support?

If you increase the amount of children that receive child support using the button, then the current child support (from Germany) is automatically calculated.

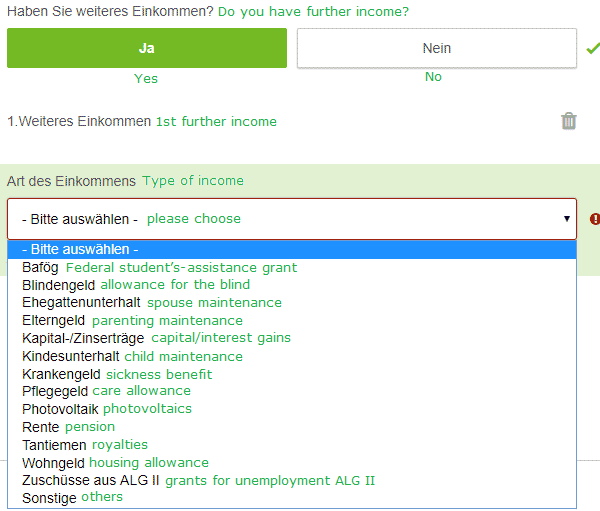

Do you have further income?

State all income that you receive. This option can be repeated for every different income. Each income helps you in the expenditure account. Please always remember- Everything must be provable!

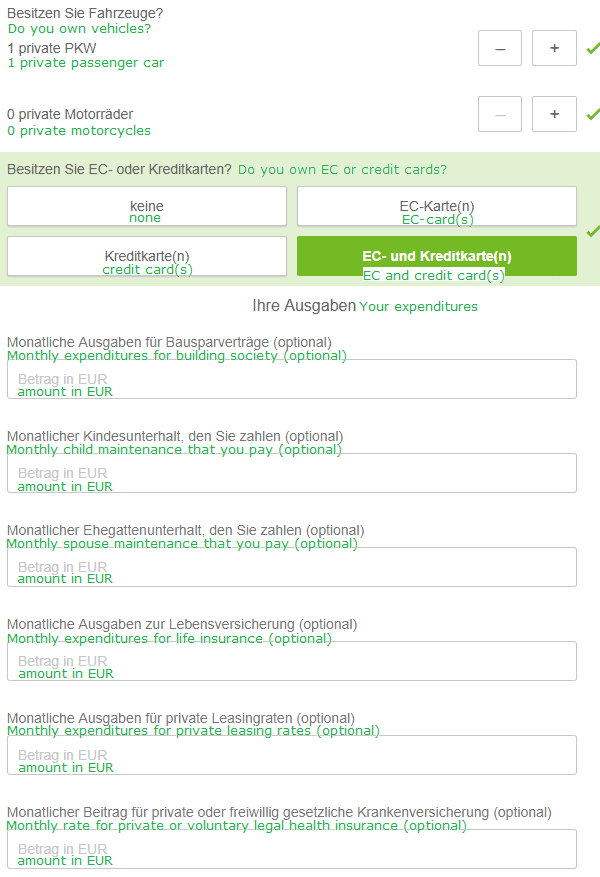

State your expenditures:

The expenditures per car or motorcycle are calculated with a lump-sum. Other expenditures are optional or are only stated, if they apply: building society rate, child maintenance, spousal maintenance (if living separately), life insurance rate, leasing rate(s), health insurance only at officers and self-employed persons (at the others it is already deducted from the income).

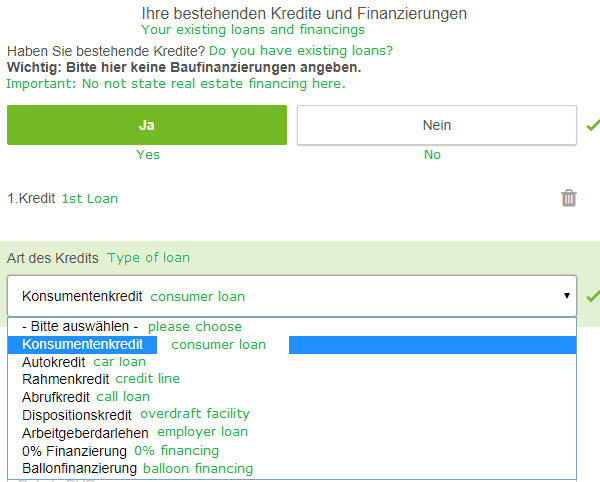

Do you already have loans?

If yes, then only state loans that are mentioned here and are entered in the German Schufa.

Exception: no financing for real estate. These offset with the countervalue/rent savings/rent payment .

Details about the existing loan:

State the existing amount of loan, the monthly installment and the expected end of the loan. If you want to discharge the existing loan with the ING, then click on “Ja” (yes) at the corresponding question. Then the bank data of the old loan is stated there for the special repayment. At “Nein” (no), the existing loan will coexist with the new one.

If you have more than one active loan, click on the green button and you can enter another one.

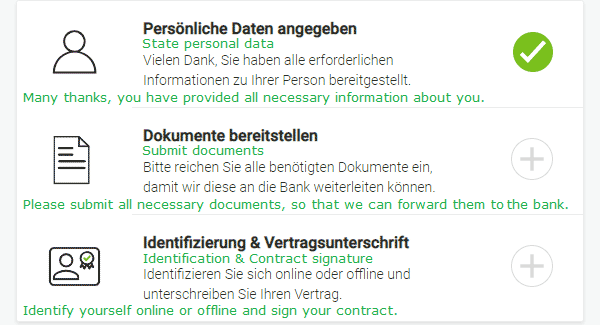

You are finished soon…

Please click …

Page 6

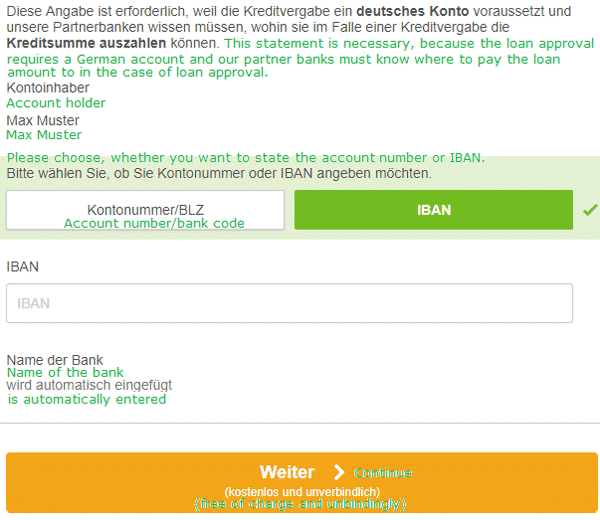

To which account should the loan be paid?

Please enter your account details to where the loan should be paid. It must be a current account in Germany, as the monthly installments will be debited from there.

You do not have an account in Germany yet? You can change that with this provider within 2–5 minutes.

Page 7

C) Initiate the loan payment

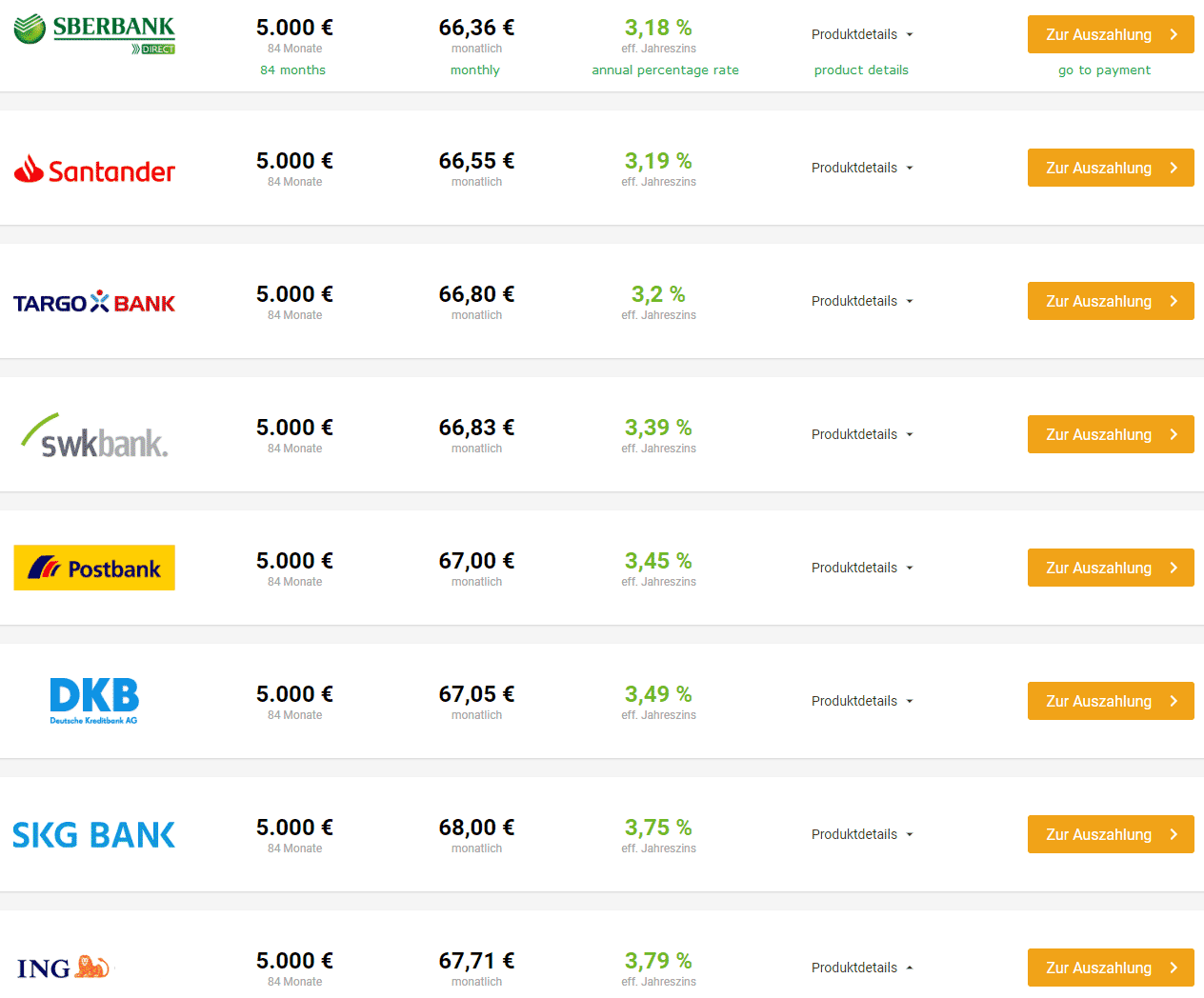

The loan calculation can take up to one minute. The result could look like this. Agreed? Then click on zur Auszahlung (go to payment).

The next steps

Documents such as the salary slip can be uploaded or submitted by mail. Moreover, you can make your identification (legitimating) using the videochat or download the coupon for the Post office. Simple and self-explainatory.

Questions about the procedure / loan application?

Please use the comments feature at the end of the page. During the filling, a telephone number of a loan advisor is shown to you, so that you can immediately get help through the phone.

Do you want to start with the loan application now?

Did you notice something?

The yellow link-buttons do not forward you directly to the bank, but to the service provider Smava.

You can get exactly the same ING-loan through Smava , as if you would go directly to the website of the bank (https://www.ing.de/lp/ratenkredit), but you will get the following advantages on top:

- telephone filling help by a loan advisor, as soon as you are done with page 2 of the online application

- creation of a user account, as soon as you are done with page 2; that means for you that you can return anytime to the online application. Sometimes, you have to look for documents and data or you are interrupted. All your filled data will be saved and you can continue with the loan application at a later point of time

- you will receive the calculation of the comparison automatically and can see how cheap the ING-loan compared is to other banks that would also finance you. That has already been calculated.

- if the ING would not finance you, you receive immediately alternative suggestions that are calculated with your creditworthiness. This way, you can save an anew data entry at another bank.

- The complete service is free of charge for you!

In our sample case, there were also loan approvals of other banks that are even more favourable than the ING:

Would you have thought of applying for a loan at the Sberbank Direct by yourself? Probably not. You do not have to, even if there is an approval of the bank due to your data entry. You can choose freely. In the end, the interest rate (the table is arranged like this) is not the only selection criterion. The ING has e.g. one of the most generous rules at special repayments and one could even top up the loan later on!

Recommendation for you: Start the loan application through Smava:

Did it work out well?

If yes, then please write me through the comments feature for which bank you have decided for in the end.

It would also be interesting to know your amount of loan and what you have financed with it. Such information helps us to produce even better articles and instructions for our smart readership in the future.

A heartly thanks! 🙏

Does your service affect my Schufa score?

If the loan is not approved: no. If it is approved, it will be entered in the Schufa.