Comparison: DKB + ING + Comdirect

“Our” three main current account banks have adjusted their conditions in order to maintain themselves for the future. As there are partially changes on the way for us bank customers, you can see the new detailled comparison here:

DKB |

ING |

Comdirect |

|

|---|---|---|---|

| Account management fee per month | free of charge | free of charge if fulfilling one of these conditions:

If none of the conditions are met, a charge of € 4.90 applies for that month. |

free of charge if fulfilling one of these conditions:

If none of the conditions are met, a charge of € 4.90 applies for that month. |

| Application | ► online | ► online | ► online |

| Cards | |||

| Visa credit card | yes, free of charge without foreign transaction fee | no | € 1.90 per month without foreign transaction fee |

| Visa debit card | no | yes, free of charge, foreign transaction fee of 1.99 % | yes, free of charge, foreign transaction fee of 1.75 % |

| Girocard | yes, free of charge | ||

| Overdraft facility / Credit line | |||

| Overdraft facility on the current account depending on the creditworthiness and application | € 0 up to 15,000 | € 0 up to 10,000 | from € 0 upwards, no limit |

| Credit line on the Visa credit card | up to € 15,000 | – | up to € 10,000 |

| Can the credit line be increased through deposits/transfers? | yes (millions are possible) |

no | |

| Cash supply | |||

| Using the Girocard at the ATM in Germany | free of charge at ATMs of the DKB and ATMs with direct fee | free of charge at all ATMS of the ING | free of charge at every ATM of the Cashgroup |

| Limits? | at least Euros 50 per withdrawal | at least Euros 50 per withdrawal | at least Euros 50 per withdrawal |

| With the Visa debit card at ATMs around the globe | – | free of charge at all ATMs with the Visa-sign | free of charge at all ATMS with the Visa-sign |

| Limits? | – | at least Euros 50 per withdrawal | 3 × per month free of charge, then € 4.90 per withdrawal |

| With the Visa credit card at ATMs around the globe | free of charge on the part of the DKB | – | € 4.90 at all ATMs with the Visa-sign |

| Limits? | at least Euros 50 per withdrawal | – | – |

| Alternatives to the bank ATM? | free of charge with the Girocard in many supermarkets, with the DKB-VISA-card at participating Shell petrol stations | free of charge with the Girocard in many supermarkets, drug stores and in the hardware store | free of charge with the Girocard at Shell petrol stations and 13,000 partners of the retail sector |

| Depositing cash | |||

| Depositing at the ATM | at the DKB-machine 1.50 % of the amount, at least € 2.50 up to a maximum of € 15 | free of charge at the ING-depositing machines | 3 free deposits per calender year at depositing machines or free of charge at the counters of the Commerzbank |

| Alternatives? | deposit with “Cash im Shop” at 12,000 partner stores per day up to € 999, fee of 1.5 % of the deposit amount | at branch offices of the ReiseBank AG up to € 25,000 (no coins); fee: € 7.50 for every initiated € 5,000. | – |

| Custodian fee | |||

| Custodian fee | balances beyond € 100,000 0.5 % per year for accounts opened from December 12, 2020 | balances beyond € 100,000 0.5 % per year for accounts opened from November 4, 2020 | balances beyond € 100,000 0.5 % per year for accounts opened from January 17, 2020 |

| Account management and communication | |||

| Online banking | yes | ||

| App banking | yes | ||

| Telephone banking | no | yes Mon–Sun around the clock |

yes Mon–Sun around the clock |

| Availability of the customer service | through telephone (03012030000), e-mail Mon–Fri 7am–7pm |

through telephone (06950500108), e-mail Mon–Sun around the clock |

through telephone (041067082500), live chat, e-mail, contact form Mon–Sun around the clock |

| Supplementing services | |||

| Apple Pay | yes | ||

| Google Pay | yes | ||

| Optional joint account or authorized persons | yes | ||

| Call money (savings account with immediate availability) | yes | yes Extra-account |

no |

| Fixed money (savings account with fixed term) | yes | ||

| VWL-Sparen (savings subsidised by the state for certain income groups) | yes | ||

| Securities account | yes DKB Depot |

yes ING Depot |

yes Comdirect Depot |

| Installment loan | yes, from € 2,500 up to 65,000 | yes, from € 5,000 up to 65,000 | yes, from € 5,000 up to 50,000 |

| Further financing possibilities |

|

|

|

| Account opening | |||

| Residence | Germany, Austria, Switzerland and possibly German expats around the globe | Germany | Germany, Belgium, Netherlands, Luxemburg, Austria or Switzerland. |

| Legitimating | Online-legitimating through Video-Ident or Post-Ident | ||

| Start the account opening |  (read further information) |

(read further information) |

(read further information) |

Are we facing worsenings?

Yes, in some points the conditions really became worse.

Compared to banks that do not have such a condition-sensitive clientele like the Sparkasse and Volksbank, it looks quite good at our directs banks.

The three banks still are in competition to each other and this is our guarantee that the conditions will remain bearable. If at some point only one big player is left (factual monopolist), then it can dictate the prices regardless of outflows.

Let’s support the diversity of banks, always having an account at the best banks.

Examples of worsenings

-

DKB uses the “Pandemic” to limit the service hours dramatically.

This is rather weird, because there are companies that have extended their working hours in order to have the least possible amount of people working during service hours. Initially, the bank said that this would only be temporary during the pandemic.

However, it looks like the bank got used to the telephone availability on weekdays between 7 am and 7 pm. By the way, the bank is frequently not available, because the telephone lines – that were already congested before – did not improve due to the timely limits.

This is personally my biggest point of critique towards the DKB. From my point of view, it has abandoned a big advantage compared to all banks with the usual service hours. Being honest means also including that many DKB customers did not even notice the change, because they do not call the bank. They prefer to write an e-mail or there is no need to reach the bank personally.

-

Tendency towards the elimination of true credit cards?

At the Comdirect, there is the Visa Card with an individual credit line for Euros 22.80 per year. Instead, a debit Visa card is offered free of charge. Some won’t recognize any difference in it, but others know that it is a factual lowering of the creditworthiness of the customer towards payment partners. People, who reserve hotel rooms and at car rentals, know the difference.

If you do not do such things, then it really does not make a difference to you.

On the other hand, it is worthwile taking a closer look at credit cards of solely credit card companies in the future. For example Barclaycard.

-

Fees for people with money

No matter, whether you want to withdraw or deposit money or simply have more money than the existential minimum in the account, you will have to pay more fees than today.

Yes, this statement goes beyond the current price listings. At this point we think that there will be further worsenings in the future. Anyway, it is the declared goal of the politics since years to make money/cash less attractive little by little.

The banks like to play along, because cash actually is more expensive. Well more expensive than solely money in the books. This also became more expensive through the perversion of the deficit interest, this is why we have the “custodian fee” – similar to the income tax, which was formerly only for the very rich, then step by step everyone, who does not only live from the system, had to pay it.

Good news: Free of charge without minimum incoming money flow ► www.dkb.de ✅

There is also something positive!

The universe always thinks of a harmonic balance. That means that if something gets worse, something else has to become better.

For people who want to hear it rationally: If there is a movement somewhere, there is also a countermovement.

-

All three current accounts continue to be free of charge, if:

you send a standing order of Euros 700 or more in a circle.

If the incoming money flow is below Euros 700 at the DKB, the account management fee won’t apply either, as with the competitors ING and Comdirect, but you won’t have the privileged status of “active customer”.

-

Get cash free of charge at the supermarket ALDI

Not mentioned above, but possible in practice is the cash pickup of up to Euros 200 at ALDI. I have tried it last week with the DKB Visa Card and it worked fabulously. There are no fees for that.

-

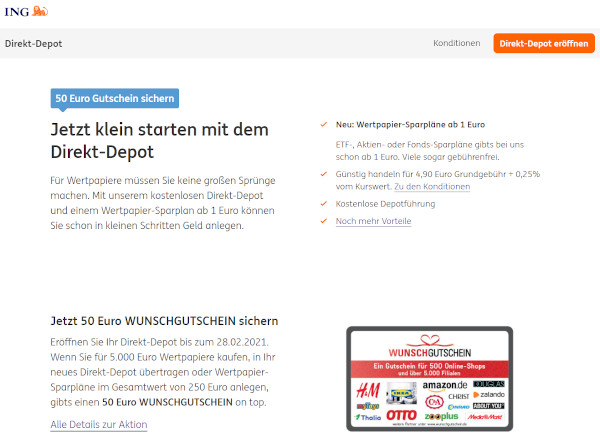

Securities accounts become more attractive

The ING suprises with the announcement of rearranging savings plans of 800 ETFs free of charge from April on. Up to now, the implementation cost 1.75 per cent in fees. The ETF-savings are possible from only Euro 1 per implementation.

Good news: ING-Depot (securities account) becomes more attractive (for small savers and big savers) + currently a Euros-50 voucher for the securities account opening ► www.ing.de/lp/direkt-depot/ (= if you want to become a new customer of the ING, then first through the securities account and then follow up skillfully with the current account!)

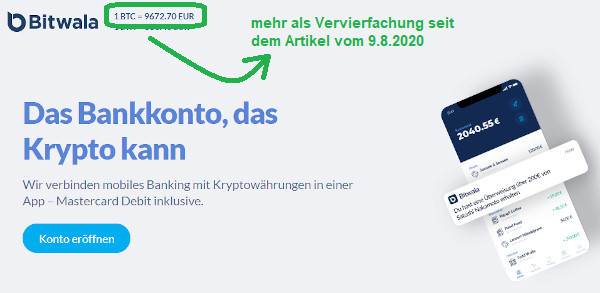

… and there’s another winner!

There is the claim:

- Does this also apply to a currency?

- Is the main character of Bitcoin really a currency?

Does the Bitcoin now daily rise with several hundred Euros?

Anyways, there is a waiting line that grows for the free current account of Bitwala, with which you can manage the Bitcoin comparably easy.

Whoever dares to switch his/her current account to such a provider, is also rewarded with a free current account. However, there are no comprehensive services like with our established banks in the comparison above.

In any case, it is a solid cost-free secondary account for bank customers, who do not want to make the standing order-circle and want to leave a bank that has introduced account management fees.

Want to try it? ► www.bitwala.com ✅

What do you think of it?

Your point of views are welcome using the comments feature.

- Perhaps you will switch to one of these direct banks due to our new comparison, because your current bank has “tightened the screws” even harder?

- Perhaps you will cancel an account, because you have only used it very little?

- Perhaps you are satisfied with a less comprehensive, but free online account as offered by e.g. Bitwala, Vivid or Tomorrow?

Do you already know…?

- Schufa-free: Secret loan from a foreign bank

- Insolvency consultants recommend already now: Open a “P-account” (seizure protection account)

- Is the Quantum Financial System around the corner?

PS: What does the author do?

Whether I would open all three accounts of the comparison still today, I do not know. They have grown to me historically and fulfill one or several functions. At the current point of time, I will keep them and let the money circulate.

Leave a Reply