Savings Accounts in Germany

Introduction: The fear of inflation remains subconscious in German society, as there were two large inflations with a total (1923) and a very strong (1948) inflation in the previous century. Thus, especially older people choose gold and real estate as an alternative form of saving in addition to savings accounts.

With the federal bank (Bundesbank), a stable monetary policy could establish in Germany and the D-Mark became one of the strongest and most stable currencies in the world for decades.

The lax monetary policy of the European Central Bank could so far not change the mind of German people about their favourite investment product, the savings account (Sparkonto).

On this page, you will find all important details about savings accounts in Germany

3 different types of savings accounts

Savings accounts can be divided roughly into three different types:

- Bank book (Sparbuch) (modern: Savings card (Sparcard))

- Call money account (Tagesgeldkonto)

- Fixed deposit account (Festgeldkonto) (sometimes called time deposit (Termingeld))

Each savings account is presented in detail and their advantages and disadvantages are discussed.

1. Bank book

DThe bank book savings account is the historically oldest in Germany. Previously, the conditions were even controlled by law. This law has been repealed long ago, but some parts of it have been committed to date by banks in their bank conditions.

- No minimum investment amount (Mindestanlagesumme) (amounts of Euros 0.01 up to several million Euros can be deposited)

- The balance bears interest (the interest rate (Zinssatz) differs from bank to bank, but is quite low)

- The period of notice (Kündigungsfrist) is 3 months; Euros 2,000 can be withdrawn each month without cancelling the bank book.

- Free account management (Kontoführung)

Almost every bank opens savings accounts for German as well as for foreign customers.

Savings Card (Sparcard) – the modern form of the bank book

As the bank book was not as interesting after the introduction of the call money accounts (next introduction) at the end of the 1990s, and many consumers switched from the bank book of a local bank to a call money account of an Internet bank with higher interest rates, some banks continued to develop the bank book into a savings card (Sparcard).

The Deutsche Bank does not provide the best offer; however, it knows how to make good ads.

Instead of a small booklet, as it was common in the bank book, one now has a savings card in bank card format. With this card, one can withdraw cash at the ATM, but cannot pay directly in stores.

Some banks even offer abroad cash withdrawals free of charge.

Advantages and disadvantages of bank books / savings cards

|

|

2. Call Money Account

The call money account is a further development of the bank book. Call money accounts are managed primarily online. There is neither a booklet nor card for this account.

The depositing is made via bank transfer (Überweisung) from a current account (most banks do not care who the owner of the money-sending current account is). Refunds are only performed to the current account of the holder of the call money account that was consigned at the call money bank. This current account is called the reference account (Referenzkonto).

General conditions of call money accounts

- No minimum investment amount (amounts from Euros 0.01 up to several million Euros can be deposited)

- Balance usually bear more interest than at the bank book

- No period of notice (you can transfer your money any day in the full amount to your reference account)

- Free account management

Not every bank in Germany offers call money accounts. Call money accounts are primarily found at online banks, with the differences in the applied interest rate and the frequency of interest credits (daily, monthly, quarterly or annually).

One can find quite a lot of foreign banks in Germany that offer call money accounts, often with higher interest rates than German banks. These foreign banks came to Germany to gather savings deposits (customer deposits). Germany is a nation of savers!

Advantages and disadvantages of call money accounts

|

|

⇒ See the call money account comparison

Call money accounts are managed through online banking by the customer himself. However, the payments can only be made to the own current account or transfers within the bank network (other call money account, fixed deposit account).

3. Fixed Deposit Account

The fixed deposit account differs from the savings account in the availability and the minimum investment amount. In the fixed deposit account, one concludes a contract with the bank, which specifies how long the money stays in the bank and the interest rate you get. That is why banks often call it time deposit.

For example, one concludes a fixed deposit contract with the bank in the amount of Euros 5,000 with a term (Laufzeit) (= duration of the investment) of 2 years and receives an annual interest payment of Euros 100. That would be an interest rate of two percent.

Terms from one month until ten years are possible in Germany. However, most contracts are concluded from one to five years. During the term, one cannot access the money. In return, the interest rate is usually higher than at the call money account, because you waive on the daily availability.

It especially makes sense to set up a fixed deposit account, when one fears a future lower interest rate level and does not need the money temporarily. The agreed interest rate upon contract conclusion stays the same at the fixed deposit account. At the call money account, the interest rate changes depending on the market conditions.

Pay attention to the expiration date of the fixed deposit account

Advice for the Fixed-Deposit: mark the end of the term in your calendar.

Some banks set the fixed deposit account – in the above mentioned example, after two years – automatically again to two years after the contract expiration, if you do not cancel.

This is done at the currently applicable interest rate. This can be better or worse than today. Other banks transfer the money back or “park” it in a daily available call money account.

At best, you write down the expiration date of a fixed deposit account in a long-term calendar and ask your bank on what happens afterwards.

If the bank conditions intend an automatic reinvestment (Wiederanlage), then write one day after the account opening a notice of cancellation (Kündigung) for the expiration date. This way, the bank can not invest again!

Advantages and disadvantage of a fixed deposit / term deposit account

|

|

⇒ See fixed deposit account offers in comparison

Frequently asked questions about savings accounts

a) Safety of savings accounts

The money in savings accounts is a completely secure investment. By law, the accounts are secured with Euros 100,000 per account and per person (= Euros 200,000 at a joint account (Gemeinschaftskonto) with two account holders). This is the minimum security amount that the European Union has established.

The account balance is more secure in Germany than in most other EU-countries

Additionally, most German banks have joined private or public deposit insurers. This way, account balances are secured up to millions (private sector, e.g. Comdirect Bank) or up to an unlimited amount (public sector, e.g. DKB).

Even if the Euro zone should break apart, the money would still be in good hands with a German bank, because one can assume that because of the economic strength, Germany will have a stronger new currency than countries in southern Europe.

The only thing saving accounts are not protected of, is inflation.

b) Taxation of savings accounts

In Germany, interest income earned on savings accounts is subject to taxation (not the account balance, only the interest!).

The tax is called “settlement tax” (Abgeltungssteuer) and is composed of 25% standard income tax (Einkommenssteuer) plus 1.375 % solidarity tax contribution (Solidaritätszuschlag) (because of the German Unity of 1990) and members of the Catholic or Protestant church depending on the federal state respectively 1.9608 % or 2.1996 %. Altogether, this is 26.4 to 28.5 % taxes.

That means that of Euros 100 interest without church membership, about Euros 26.40 are paid to the state and you keep Euros 73.60.

Tax exemption (Steuerfreibetrag)

The German tax law is supposed to be the most extensive of the whole world … therefore, also tax exemptions for interest exist. The main exception is called “tax exemption”.

Any person can use this tax exemption. It is currently (as of 2015) at Euros 801. This means: the first Euros 801 of interest is tax free.

In order to use this tax exemption, one must consign an “exemption order” (Freistellungsauftrag) at the bank. For details on this, please contact your bank.

Once everything is set up correctly, the tax for the customer is very simple, because the bank calculates everything. As a customer, you receive all interest up to Euros 801 (or at several banks up to the amount that you have consigned in the exemption order) tax-exempt credited to your account.

If your interest is more, then the bank transfers the tax for you directly to the tax office (Finanzamt). You do not have to worry about it.

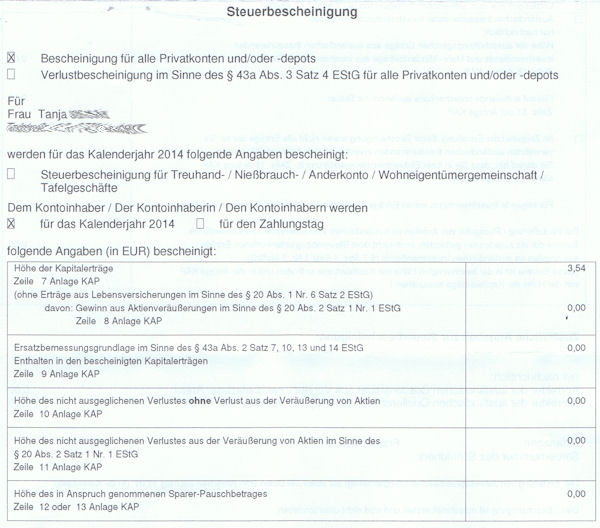

In both cases at the beginning of each year, you will receive a tax certificate (Steuerbescheinigung) from your bank from the past year, in which all the required information is stated. This is included as an attachment to the annual income tax return (Einkommenssteuererklärung).

Typical tax certificate of a bank for capital gains (interest)

Non-resident tax payers in Germany

If you are not subject to tax in German, because you are taxable in another country, then all interest income is tax free. For this, your status as a non-resident taxpayer (Steuerausländer) must be consigned at the bank; otherwise the tax will be deducted automatically.

Here you can find more Details about non-resident taxpayers in German language.

c) Foreign directs banks in Germany

Foreign direct banks often offer higher interest rates than German banks, as they have come to Germany to gather money. The classic aspect of these banks is that they only offer savings accounts, but no other banking services.

The deposit insurance is often in another EU-country.

As one focuses on winning customers in Germany, these banks do usually not accept customers residing abroad. In part, the problem is that the software of the bank can not make a distinction between resident taxpayers and non-resident taxpayers.

The Rabobank from the Netherlands, for example, is one of those foreign direct banks that gathered billions in German… however, only accepts customers with their place of residence in Germany (resident taxpayers).

d) Savings accounts for companies

Of course, savings accounts can also be opened in the name of a company. Unfortunately, the offer and the interest rate are not as good as for private persons. Additionally, in Germany there are pure retail banks that do not open company accounts.

Moreover, it is a pity that the banks of companies usually want to see a German address and, if applicable, a registration in the commercial register.

However, I will be happy to investigate other banks, at the request of abroad companies that want to invest money in Germany.

Account opening in Germany

Opening a savings account in Germany is relatively easy, as you provide money for the bank and not vice versa. Thus, no creditworthiness check of the customer applies.

You simply visit the branch office of a bank with your ID card or passport and open a savings account. If you value a good – or the best – interest rate, I recommend you to compare the interest rates in advance.

All accounts of the two comparisons can be applied for online, if you have an address in Germany.

It could be a strategy to first open a savings account at a good bank and later open a current account too, in order to obtain a better rating in the creditworthiness check. I describe this strategy in detail in this article.

Summary

Opening a savings account in Germany is easy. It can take place in a branch office or online. A legal requirement is the identification of the person.

Savings accounts differ substantially in the term of the investment:

- with a 3 months’ notice from Euros 2,000 (bank book, savings card)

- daily availability (call money)

- availability at the end of the agreed term (fixed deposit)

The interest income from savings accounts is taxed generally. Exception: tax exemption or non-resident taxpayers.

It is a good idea to have a savings account in Germany!

Hello,

I have Italian nationality but I don’t have bank account in Italy. I’m working in Kuwait and I have bank account in Kuwait. I would like to open an account in German bank to transfer monthly my salary and save it. Would you advise me if I can do this.

Thanks and Regards

Fine. That is an interesting issue / challenge! We will make practicable advice and will post it here in the next days.

Today we publish the article with the answer to your question. I hope that helps.

https://www.deutscheskonto.org/en/account-opening-in-germany-from-kuwait/

I am in Australia and will be travelling to Europe, I have at Deutsche Bank Sparbuch since 1986. To withdraw money from this account away from Germany I need a bankcard, access or sparcard? Can I get that?

Thanks

Glenn

Australi

The former Sparbuch is the SparCard by Deutsche Bank now: https://www.deutscheskonto.org/en/deutsche-bank/sparcard/

We are not Deutsche Bank, so it is better to ask this bank direct.

Dear Tanja

I am interested in opening a bank account (savings or current) in Germany which I can use to trade shares in international stock exchanges. I am a South African citizen living in South Africa.

Can you please advise me if I can be permited to open an account, and if so, how much do I need as a minimum to open such an account

Savings accounts are described in detail on this page. Securities account or traders accounts not yet, so currently, we cannot provide you with any recommendation.

Dear Tanja

I am interested in opening a bank account at Commerzbank I am a polish citizen living in Russia,

What is the size of bank fees when I withdraw money from ATM abroad using debit bank card?

Sorry, I cannot support the Commerzbank, as I am not a customer of this bank and it is not one of the banks we observe. Please contact the bank directly.

Can you please send me the link in opening the account online? I am applying for a student visa and opening an account is one of the requirements of the embassy however I cannot find the link to change the language from german to english. Thank you for your assistance

Sorry, blocked accounts are not the topic of this webportal.

Can I open an account in other currencies such as the US$ or the UK Pound?

Sorry, but savings accounts in other currencies are outside the purview of our web portal, so we don’t have any particular knowledge in this area. We do have an article though, that deals with the subject: https://www.deutscheskonto.org/en/dollar-account/

Thanks you for the useful information, I was wondering if there are limitations on who can open bank accounts in Germany. Students on temporary visas for example? Tourists? Etc.

This is handled differently by the different German banks. The best would be if you asked the bank you’d prefer directly. Good luck!

HI, I opened an aaocunt with DB in germany and I receive a Konto card and spare card. I also see that in my online banking. Is my Sparecard a saving account? Can I transfer money from my Konto account to this spare account and keep it as savings or Do i have to open another saving account? Thanks for your reply.

The “Sparcard” is a saving account. Contact your bank for using details, we can only support “our” banks, because have no bank account at Deutsche Bank (any more).

Good day,

Would you be so kind to confirm? As I get this, if you put a 1000 EUR on my savings account and I get a 100 EUR from my savings, only 100 EUR will be taxed ?

Best regards Mark

Hey, hey! In Germany, only the interest gained from a savings account is taxed – but not the deposits and withdrawals.

Thank you very much. Could you be also kind to tell me is there any insurance on your sum of savings or insurance for money in case if something happens?

In Germany, deposits on checking and saving accounts with an amount of up to EUR 100.000 are guaranteed by the so called “Einlagensicherungsgesetz”.

Also would you be so kind to tell about the sum over Eur 100.000 is that also guaranteed?

Good day, I would like to know whether i can use savings account to receive monthly salary. Moved to Germany couple of months ago as jobseeker, relocated within Germany as i landed job in diff city, still dont have local address in new city. Local registration i have is from old city couple of months ago. Banks are not accepting it.

Yes, receiving the salary on a savings account is possible. These accounts are called “Tagesgeldkonto” or “Sparbuch” in German. There are also savings called “Festgeld”, where it is not possible.

Hi!

Just have a question to clear any doubts if you don’t mind advising me as I find the banking system in Germany very confusing.

I am a Malaysian moving to Germany as my husband lives there.

My question is, as I surely will have to open a savings account, will my monies be deducted eventhough I’m not earning? Example if I have €10,000 in my savings account, will any sums be deducted?

Thank you in advance. Your answer is much appreciated!

Hi!

We cannot quite follow your thoughts/concerns – maybe the banks in Asia actually do work differently from those in Europe. Anyway, each bank has their own Terms & Conditions. Once you have selected a bank, you can find these at the “Preis- und Leistungsverzeichnis”, so you can be on the safe side.

I am thinking about buying a Bed and Breakfast in Germany. I want to open a bank account (interest gaining) to put money in to be used when I get there in 2019. What do you recommend as my course of action. I am in the United States and will be sending money to Germany to save and hold for business purchases in Germany.

The interest is much too low to make money off it – regardless of which German bank. Our central bank currently has a key interest rate of -0.4%. Please note the minus in front of the number!

It would be best of you opened a (savings) account at a bank, that opens an account for you as a US American and which you can manage comfortably.

Which German banks will open a savings account for an American that will be moving to Germany and applying for citizenship in Germany?

There are many banks that open savings accounts for foreign citizens, though only after they have an address (residence) in Germany.

Please I wanted to ask what Bank account is good for beginners investors in Germany?

Comdirect Depot ► http://www.comdirect.de/depot.

Hi Tanja,

Thank you so much for taking the time to write this article. Very helpul.

Question, is there a tax treaty between Canada and Germany in regards to investments: Savings, capital gains, dividends?

Also, do you know any accountant that is familiar with cross border taxes between: Canada and Germany.

Thanks

Hi Car,

Yes, there is a double taxation agreement, but we do not yet have a specialized expert re. that on our team. You might want to google CPA “Andreas Hintz”, who is open to such topics.

Hi,

What options are there for a USD savings account?

I have some USD in a foreign bank and would want to bring them in Germany (as I currently live here) but my current bank (DB) only offers a USD checking account that costs 12 EUR/month….

Thanks,

urweiss

The article is already a bit older, but it might help: https://www.deutscheskonto.org/en/dollar-account/

Dear Tanya,

Thank you for a very informative article. I have a question regarding fixed deposits: What is the penalty for early withdrawals and to what extent does the German law protect a customer who wants to terminate a long fixed deposit?

Thank you very much!

Best wishes,

Diana

Usually you cannot access the money before the end of a time deposit. One has concluded a contract, after all!

There are no general rules for early termination for all banks. Some banks have their own rules. For example, that you have to forego the interest of the current period. There are also banks that are more accommodating. That is all individual. Just talk to your bank “smartly” if you want to access your money before the due date.

Hi Tanja,

I have a DKB account and I am not a resident in Germany. In the article you say “In Germany, interest income earned on savings accounts is subject to taxation (not the account balance, only the interest!).” Does that mean that it does not matter the amount, I won’t pay taxes for my savings?

Thanks a lot

1) If you do not live in Germany and are not taxable in Germany, you can be exempted from the automatic tax deduction. Please clarify this with the bank directly.

2) If you have money only in the checking account, you do not need to worry: There is no interest there and therefore there is nothing to tax.

3) If you have a balance on the Visa Card, you will receive 0.2 percent interest. It is probably not noticeable at all when taxes are deducted. The inflation rate is much higher!

Currently I am Germany. If I invest in 30000 euros, for 3 years or 5 years, how much money will I get each month. I can not allow permission to stay in Germany. Please let me know

This is an editorial web portal, but not an investment consultancy. Best of luck for finding a good consultant.

What can be maximum interest percentage I can get if I am on study visa? I just want to have an idea of expected income by saving account.

The amount should be ready to be withdrawn if I need.

Thanks in advance.

This is currently completely uninteresting in the Euro zone, since for years the central bank has been lending money to 0 percent. People in Germany currently make easier income by renting out apartments or getting dividends on stock shares.

Very nice article!

Would you know if the same tax law applies to a German resident who would have invested in Bank fixed Deposits in India? Same Tax Rate and Tax exemption?

The allowances and the tax rate are the same for a taxpayer in Germany – regardless from which country he receives the interest. In the income tax declaration, however, the fields are different ones (investment income from Germany / abroad).

hi which bank in EU gives best interest rate ?

Hello,

I was wondering if you can advise on my below issue.

I left Germany at the end of 2020 where I had 3 bank accounts with Unicredit Hypovereinsback (2 saving accounts and 1 Girokonto). I asked to close all 3 of them a few weeks ago and they said they will send me 3 closure forms by email. Since I didn’t receive anything for about a week, I followed up and then they sent me only one cancellation form for my Girokonto.

When I asked where are the forms for closing the saving accounts, they said the accounts have zero balance (which I was aware of) without further addressing my question.

I signed and sent back the form to close my Girokonto, asking again when they’re going to close those 2 saving accounts. Another few days passed without an answer, so I followed up again.

This morning I got a reply, saying that in order to close those 2 empty accounts they want me to send them “den letzten SB Sparauszug im Original”.

Apart from not telling me this from the get go and their poor customer service, which is terribly annoying, how can I actually close these accounts? I never had a Sparbuch so I’m not sure exactly what they’re asking for. Plus don’t they have all the evidence/information they need in their database?

Is there any other way to close a saving account stress-free, while no longer living in Germany?

Any feedback will be much appreciated.

Thanks,

Anca

Yes, you don’t need a form to cancel one or more bank accounts. A very simple “three-liner” is enough. For example, in German:

Simply print it out, fill in the IBAN, sign it and send the original to the bank by letter.