How to get an installment loan easily + cheaply in Germany!

At least 50 per cent of all loan applications are rejected!

So that your loan application will be approved and that you, being a smart bank customer, pay less interest than other people, we have developed this page for you.

Idea and strategy using the example of the ING-DiBa:

|

||

| Loan type | installment loan (German: Ratenkredit) |

Housing loan (German: Wohnkredit) |

| Effective interest rate | 3.79 % | only 2.99 % |

| Application | ► online | ► online |

Comprehensive details in the course of the article!

The most important facts summarized for you:

-

Choose a bank with a long term + special repayments

What many people do not understand: Not the creditworthiness (Schufa-score) or the income is decisive for the loan approval, but the amount of the monthly installment according to the creditworthiness and income!

In other words: Many would get a loan, if they would just choose a longer term and by this a lower monthly installment.

Why is that so?

-

Every bank works with a fictitious expenditure account, in which your income as stated is the starting point. Then, quite a lot of lump sums for lifestyle, children, living, etc. are deducted. The (fictitious) amount of freely available money remains. The monthly installment plus a safety margin for unpredictable expenditures should be able to be deducted from this amount.

With every Euro less, your chance of the loan approval rises!

-

Banks want and must earn money with the loans. No matter how high the loan is or how long the repayment will take, the costs are quite the same. With longer terms, the bank earns more money, because you pay interest for a longer time.

You, being a smart bank customer, can take advantage of this fact, if you conclude your loan at a bank with a generous right on special repayments. More about this subject in a second!

-

-

Choose a bank with an offer of housing loans, if you are a real estate owner

The first point applies to everybody, this is only another option for perhaps 10 per cent of our readers …

What again many do not know: The use of the money paid of a housing loan is not checked.

That means: You can improve your residential property with the money, but you do not have to. You can also use the money to fund a sideline business or go on vacation … but just the fact that you are a real estate owner will help you to get a significantly cheaper interest rate. Details on that in the course of the article!

Want the explanation of the article as a video?

installment loan and housing loan in a comparison

|

||

| Loan type | installment loan | Housing loan |

| effective interest rate | 3.79 % | only 2.99 % |

| possible loan amount | Euros 5,000 up to 50,000 | |

| Repayment | 2–7 years (fixed monthly installment) |

|

| Special repayments | anytime, as often and as much as you want (will shorten the term) |

|

| special requirement | – | existence of a real estate property |

| Application | ► online | ► online |

Clarification whether the housing loan is a possibility for you?

Apparently, there are only two differences between an installment loan and the housing loan

- the housing loan is about ⅓ cheaper,

- the requirement is a real estate ownership.

Everything else does not matter!

What is valid as a real estate and what has to be proven?

The proof that you are a real estate owner is super easy. Just a copy of the last tax notice or a copy of the land register has to be added to the loan application.

It does not matter:

- whether you have already paid the real estate

An existing real estate financing does not affect the housing loan and is not stated in the loan application (as other people have to pay rent; that is cancelled out). - whether you live in the real estate yourself

For example, you are renting a house, but you have a condominium as a capital investment > the rented condominium entitles you to take the housing loan. - The type of the real estate

House, appartment or undeveloped land? Everything is okay, if the proof has your name on it. 🙂 - The value of the property

As the loan is not secured with the real estate – there is no entry into the land register –, the value of the real estate does not matter and does not have to be stated at all. A lot in a cheap region would be enough. - Where the real estate is situated

The property can even be abroad (e.g. finca on Mallorca or holiday home in Florida). A suitable proof of the ownership must be provided. But please note that your main place of residence and your main source of income must be in Germany.

If you want to apply for the loan together with your partner – that increases the probability on a loan approval even more –, and it is enough, if one of the two borrowers is a real estate owner.

Important to understand: The use of the housing loan is intended for improving a property (e.g. new kitchen, new bathroom, create a garden) – however, the use of the money is never ever checked by the bank!

Everything that follows applies to the installment loan and housing loan …

Increasing the probability on a loan approval

As announced above in the article, there is a method with which you can considerably increase the probability on a positive loan decision!

Basically, the method consists of the following formula:

Longer term = lower installments = higher loan probability

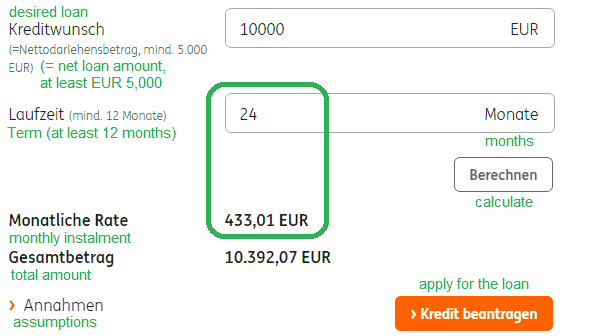

Let’s stay with the example of the ING-DiBa (2 years term):

If you want to repay the installment loan in the amount of Euros 10,000 with a term of 2 years, the monthly installment is Euros 433.01 (housing loan: Euros 429.60).

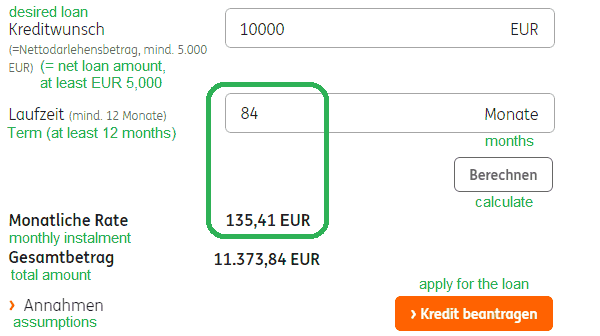

At a term of 7 years, the monthly installment is only Euros 135.41 (housing loan: Euros 131.90).

Same loan amount, but monthly Euros 297.60 less burden (in the expenditure account)

In this presentation, one can obviously see that the probability of a loan approval is increased by the reduction of the monthly installment.

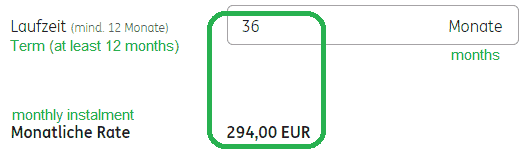

For the following example, we do not take the extreme of 84 months instead of the 24 months, but 36 months (3 years), because many people really finance with a term of three years. This is a comprehensive period of time.

Financing plan for you to imitate:

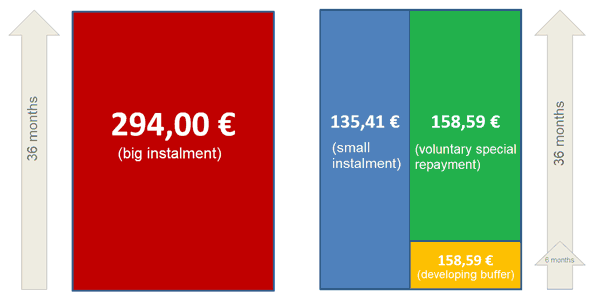

| common financing | smart-bank-customer-financing | |

| Loan amount | Euros 10,000 | |

| applied for term | 3 years (36 months) |

7 years (84 months) |

| actual term | 3 years (36 months) |

|

| monthly installment | Euros 294.00 (loan installment) | Euros 135.41 (loan installment) Euros 158.59 (savings installment or special repayment) |

| Probability of a loan approval | averagely good | considerably higher (!) |

| Apply for the loan online | ||

| ► installment loan (for everybody) |

► Housing loan (for real estate owners) |

|

| We have chosen the Euros 10,000 for you for the easy visualization. If you want to finance e.g. Euros 25,000, then you simply multiply the values in the table with 2.5. Please give me feedback through the comments feature, whether you use our plan or what individual changes you have made. This way, we can even better expand on the smart usage in the following articles. Many thanks for choosing DeutschesKonto.ORG for your research! |

||

Step-by-step instruction

-

How to calculate the loan for you

Choose the amount that you need and see, what monthly installment is bearable for you. If we stick to our example, this is a Euros 10,000 loan and Euros 300 would be bearable monthly as the loan installment. The closest is the term of 3 years with monthly Euros 294.

Screenshot of the ► loan calculation of the ING-DiBa

-

Apply for the maximum term

You apply for the maximum loan term of 7 years (84 months).

-

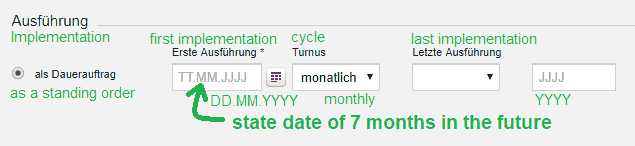

Receive the loan payment

You get paid your loan. By the way, you can fix a desired date for the loan payment at the ING-DiBa. The application is possible three months earlier. Until the payment, you do not pay any commitment interest. However, you can finish your desired financing and can rely on the available loan, and can then prepare other things …

-

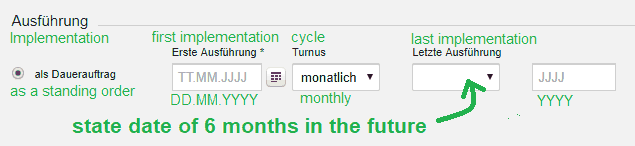

Set up standing orders for the fast loan repayment

- Open a savings account

if not available yet (this can also be the extra-account of the ING-DiBa). There, you set up a monthly standing order, in our example in the amount of Euros 158.59. You let it be implemented 6-times:

By doing so, you save yourself a buffer of Euros 951.54 within 6 months.

Being a DKB-customer, you can program standing orders for the future well!

That means for you: If something unpredictable happens in your life, then you can pay the loan installments for more than one years with this savings account! Completely independent from the other income.Isn´t that great?

Everyone, who was already behind schedule with a loan installment, knows how this feels … With our strategy, you make provisions, so that you can always sleep well!

- Set up a monthly special repayment

If your bank – just like the DKB – permits to program standing orders for the future, then set up a second standing order right away:

This is your programmed standing order for the special repayment, beginning after the end of the buffer.

You state the IBAN of the loan account as the receiver account. The transfer amount is in our example again at Euros 158.59. With this “programming”, you make a special repayment every month. This is permitted and no further costs arise by this. But you shorten your term considerably!

- Open a savings account

-

After 3 years: Get your loan to 0 with the last special repayment

If everything went according to the plan, then you transfer the buffer from the savings account to the loan account after three years, and the loan will be completely repaid and finished. Done!

Done: Loan repaid punctually and completely!

Graphical illustration for your better comprehension

Easily understandable for you?

installment loan with automized special repayment and buffer just for the case!

Not considered in the illustration: With our smart-bank-customer-method, a little more interest applies, although we have a loan repayment of three years, because we have Euros 951.54 in the buffer. This is so-to-say the price for a higher probability of loan approval and sleeping peacefully.

If you are not willing to bear these minimum interest, then just leave the buffer out. With the beginning of the immediate special repayment through the standing order, the interest burden with our smart-bank-customer-method is exactly the same as with the conventional one. I am looking forward to your feedback through the comments feature at the end of the article!

Advantages of the smart-bank-customer-method summarized:

- Higher probability on a loan approval, as there is a lower monthly burden

- Incorporation of a financial buffer, so that you can sleep peacefully, even if things in life change

- More flexibility, because it really can be that it can get tight with the “big” installment in a month – then you just skip the voluntary special repayment.

- No further costs because of special repayments

- Loan is repaid just as fast as with the conventional method, but with much more security for unpredictable events!

How the application works (step-by-step video)

► installment loan

► Housing loan (for real estate owners)

A small petition to you, being a smart bank customer

The elaboration of such instructions is a whole lot of work and requires quite some creativity and experience. For you, smart bank customer, and eventually subscriber of our Sunday-mail, we do that gladly and with pleasure!

The ideas and contents on DeutschesKonto.ORG are so good, especially because of the valuable supplements of the smart-bank-customer-community through the comments feature, that it is meaningful that even more bank customers find out about it.

Please give us the full star-evaluation and please recommend us to others, for example by passing on the link of this page. Many thanks!

Questions? Supplements?

Please use the comments feature. Thanks!

If you are not yet that long in Germany (short creditworthiness history) or you know that your creditworthiness is currently not so good, then it is recommended to find an installment loan through this ► comparison. You desired loan is pre-checked at several ones instead of at one really good bank, which increases the chances on a loan approval significantly, especially at a not very good creditworthiness.

Please also note that the requirements for an installment loan in Germany is the place of residence and a regular income in Germany. Good luck!

If I applied a loan in my bank in Germany how many working days do the bank need to approve the loan and send the money to me?

The credit check is done online directly. Afterwards, the papers need to be submitted. If there is no discrepancy, the disbursement process is started. Our quickest readers have the disbursement after 5 days.